LIFE INSURANCE

Your Ultimate Life Insurance Solution

Securing Tomorrow, Embracing Today: Unveiling Our Upcoming Life Insurance Services for a Brighter Future!

Securing Tomorrow, Embracing Today: Unveiling Our Upcoming Life Insurance Services for a Brighter Future!

A life insurance policy is an agreement between a policyholder and an insurance provider. The person makes periodic payments of a predetermined premium. On the other hand, when an insured event, such as a death or disability, occurs, the insurance company pays the beneficiaries the insured amount or the product's defined benefit upon maturity.

Life insurance works on a straightforward principle. You would have a figure in mind as the insured for which you could wish to get a life insurance policy. Remember that in the sad event that something were to happen to your family, this money should be sufficient to meet their expenses.

Based on this figure, the insurance provider will determine how much you must pay in premiums. The covered premium amount will be paid by you in either a lump payment or installments. Please be aware that the premiums must be paid for the duration of the policy, either as chosen by you at the outset or as specified by the insurance company.

The beneficiary only receives the life insurance policy amount, also known as the sum assured, upon the policyholder's passing. This will be the total assured plus any other benefits that have accumulated, if any, as specified in the policy documentation.

The ability to help build a secure financial nest for your family is the largest advantage of life insurance. The advantages never stop. You should become aware with the benefits of life insurance policies if you plan to buy a new one. Below is a list of a few:

Having life insurance gives you the ability to safeguard your family, which is one of its main advantages. In the sad event that something goes wrong, the beneficiaries can use the death benefit money to cover their expenses and not worry about meeting their life and financial goals. It should be noted that there is no tax on the death benefit proceeds in any way. Life insurance offers cash assistance in the event of an unfavorable circumstance.

Mature benefits are also known to be offered by certain policies. The family's long-term objectives can be met and their financial security can be ensured with the revenues from this payout.

Building a corpus for their future marriage or higher education, as well as reaching any other milestones specified by their parent or guardian, is the main goal of a child plan. More significantly, a child insurance plan offers a safety net in the event of an unfavorable circumstance because the majority of these plans have a premium waiver feature that relieves the insured of the financial burden of future premium payments, protecting the maturity amount.

The payout will be made in one lump payment at maturity. It is also possible for you to decide to receive the payouts periodically in order to cover certain expenses related to life events like marriage or your child's further education.

Retirement planning is crucial in a landscape without guaranteed pensions, increasing costs, and a shift towards self-reliance. Building a retirement corpus through dedicated programs is essential. This corpus is then used to purchase an annuity plan, ensuring a stable and regular pension income, mitigating the need to rely solely on others or uncertain sources in retirement.

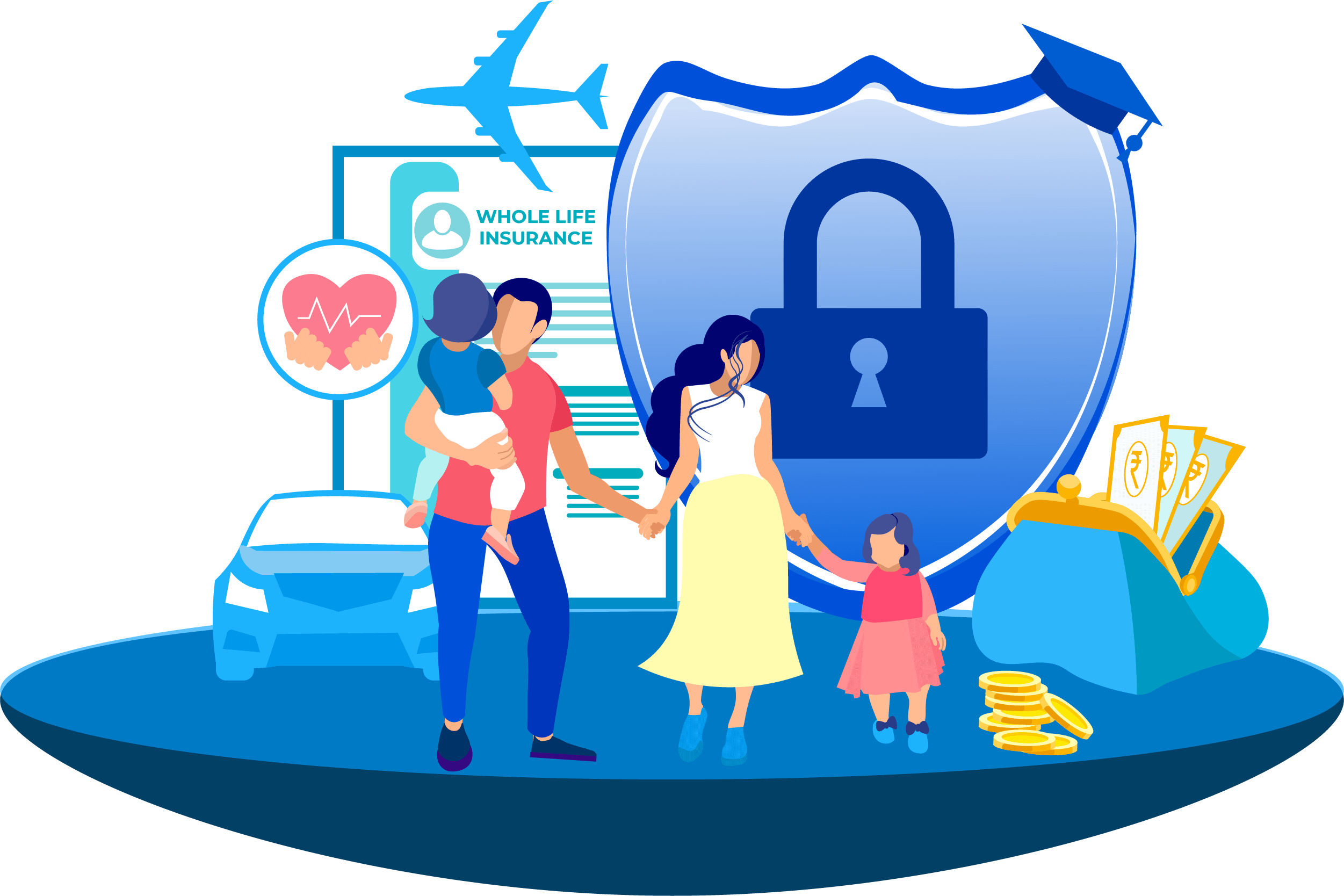

It's important to include life insurance in your tax preparation. In addition to providing security for your family's future, a life insurance policy allows you to claim tax exemptions on maturity payouts and tax deductions on premium payments.

The main purpose of life insurance is to provide financial security in the event of an unfavorable circumstance. Term life insurance policies typically provide a predetermined amount of money that protects your family in the event that the policyholder passes away.

If you are your family's only provider, one of your main concerns is how you would support them financially in the event of an unforeseen circumstance. Here's where purchasing life insurance can help reduce the danger.

The idea of life insurance is to reduce risk and give your heirs financial support so they can be taken care of in the event that you pass away

One of the most widely used types of life insurance is term life insurance. The majority of individuals select term life insurance because it offers excellent financial protection at a reasonable price in the form of a sum assured. On the other hand, if the policyholder lives out the policy term, pure-term insurance policies do not offer maturity rewards. Therefore, life insurance policies are seen as providing financial security to the policyholder's designees in the event of death within the policy's term.

Endowment policies are a particular kind of life insurance that are intended to pay out a lump sum payment in the event of the policyholder's death or policy maturity. An endowment policy can be the ideal choice if you're looking for a plan that can offer both savings and insurance benefits.

Whole life insurance is a kind of policy that protects your family for a long time by offering coverage for the entirety of your life, or up to the age of 100. For a single or short-term premium, the majority of these require payment. As long as the policyholder pays the required payments on time, the policy will stay in effect.

Unit-linked insurance plans, or ULIPs, provide both wealth building and protection. ULIPs include a variety of funds, including money market, debt, and equity. ULIP provides flexibility, such as the ability to switch between funds and liquidity through partial withdrawals, based on your risk tolerance. In addition to market-linked advantages like fund value paid as a maturity benefit, they provide a minimum guaranteed death benefit as a sum assured.

Comprehensive Insurance is highly recommended as it provides complete coverage for your car. However, for older cars, a third-party policy is a cost-effective choice, offering mandatory coverage.

Purchasing or renewing car insurance online takes a few minutes. Visit metassure.ai, input details, pay the premium, and get an instant policy.

Trim your four-wheeler insurance premium by opting for a higher deductible, installing anti-theft devices, building your No Claim Bonus, avoiding unnecessary add-ons, and thoroughly comparing plans online.

Driving without at least third-party coverage is illegal in India. Penalties include fines and potential imprisonment for repeated offences.

No, the No Claim Bonus cannot be transferred to the new owner. It remains with the policy holder and can only be transferred to the new car of the same owner

No, your personal motor insurance policy typically doesn’t cover rental cars. Rental agencies usually offer separate insurance.

Protecting your vehicle and yourself on the road is just a few clicks away. Get a free quote today and let us help you find the Car insurance solution that best suits your needs. Drive with confidence knowing that you're covered by Metassure. Your safety and peace of mind are our top priorities: